A non-state pension fund (NPF) is more than just a financial product. It is a long-term tool for building your own pension capital and can become an important supplement to the state pension.

When people begin searching for information about NPFs, a number of questions arise almost immediately: which fund is better, whether rankings can be trusted, what really matters, and how to avoid making the wrong choice.

In this article, we will explain how to correctly read non-state pension fund rankings, which indicators truly matter, which can be misleading, and how to choose an NPF that suits you personally.

The best NPF is not the one with the highest return in a single year, but the one that demonstrates stable long-term performance, has substantial assets, a large number of participants, transparent governance, and clear, understandable terms for clients.

It is the combination of these factors—rather than any single metric—that determines a pension fund’s reliability.

What іs a Non-State Pension Fund, in simple terms

A non-state pension fund is a voluntary pension savings instrument. You enter into a pension contract, make contributions, and these funds are invested in financial instruments in accordance with applicable legislation.

An NPF is not an account where money is merely stored. It is a long-term investment mechanism specifically designed to generate pension payments in the future.

Who an NPF Is suitable for

An NPF is suitable for those who:

- want to have an additional source of income in retirement;

- are ready to accumulate savings gradually, without a large initial capital;

- understand the value of consistency and a long-term horizon.

An NPF is not a tool for quick profits. It is about financial discipline, regular contributions, and trust in the chosen savings model.

Top NPFs in Ukraine: how to properly understand rankings

Rankings of non-state pension funds in Ukraine are often perceived as a direct answer to the simple question: “Which NPF is the best?” In reality, rankings are a navigation tool rather than a final verdict. The same fund may top the list in terms of net asset value, rank among the leaders by number of participants, and at the same time not be first in short-term returns. That is why correct interpretation of rankings is essential for making an informed choice.

There is no single universally best fund for everyone. However, there are objective criteria that allow you to compare NPFs and understand which one best matches your goals.

Key criteria for evaluating NPFs, or how rankings are formed

NPF rankings are usually based on objective financial indicators that can be compared across funds using uniform rules. These are the data points used by analysts, regulators, and market participants.

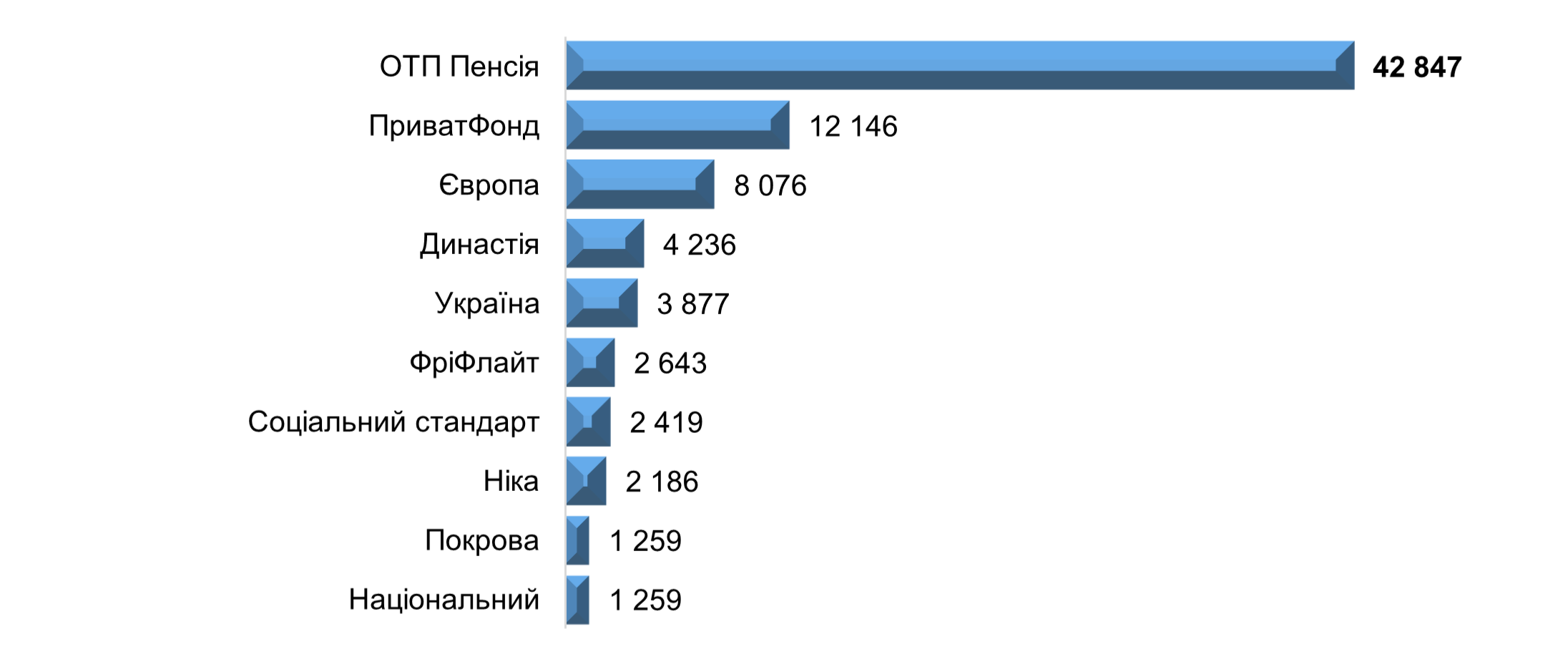

Fund assets (often referred to as NAV – Net Asset Value)

This is a core indicator of an NPF, showing the actual volume of funds working for the benefit of participants. A high NAV indicates the scale of the fund, a significant amount of accumulated capital, and trust from contributors. At the same time, NAV is not a direct measure of returns, but it provides a foundation for stable and diversified investment.

Top 10 NPFs in Ukraine by NAV as of 31.03.2026, UAH:

Data source: Consolidated reports of the National Securities and Stock Market Commission (NSSMC) and the Ukrainian Association of Investment Business (UAIB)

Number of participants

This indicator reflects a fund’s popularity. A large number of participants (whether total participants, individual investors, or institutional investors) signifies market trust and reduces the fund’s dependence on a few large contributors. Over the long term, this positively influences the resilience of the fund’s model, even though the metric itself does not describe the investment strategy.

Top 10 NPFs in Ukraine by number of individual investors as of 31.03.2026:

Data source: Consolidated reports of the National Securities and Stock Market Commission (NSSMC) and the Ukrainian Association of Investment Business (UAIB)

Fund performance (Returns)

Pure performance rankings are encountered less frequently, as not all NPFs publish results daily. Most often, performance is calculated as the growth in the value of one unit of pension assets over a specified period.

Fund performance is an important metric because it directly affects the growth of your savings. However, you should not choose a fund solely based on its performance over the past year. For pension savings, it is better to look at performance over 5 years or more, if such information is available for the fund.

Top 10 NPFs in Ukraine by 10-year performance:

Data source: Consolidated reports of the National Securities and Stock Market Commission (NSSMC) and the Ukrainian Association of Investment Business (UAIB)

What rankings usually do not take into account

Even the most detailed rankings have blind spots. Among them are:

Consistency of performance

For long-term savings, consistency is often more important than short-term records. A moderate but steady result may be more attractive than a sharp spike in performance during a single period.

Transparency of reporting

A reliable fund regularly publishes performance results, asset structure, the value of a unit of pension assets, and other key information. If basic data is difficult to find, this is a reason to ask additional questions.

Who manages the assets

NPF assets are managed by an asset management company. It is worth paying attention to its experience, approach to risk management, investment strategy, and the quality of communication with clients.

Administrator and custodian bank

In an NPF, different functions are divided among professional participants: the administrator, the asset management company, the custodian bank, and the fund’s board. This separation is a crucial part of the control system. It is important to understand who performs each of these roles.

Client convenience

Service quality also matters. Online onboarding, easy contributions, a clear and informative fund website, consultations, and access to information all influence the real client experience.

In practice, no single indicator works in isolation. A fund’s strong position is formed at the intersection of several metrics.

Comparison Table: Which Indicators Are Worth Reviewing

How a comprehensive approach looks in practice

When several rankings are analyzed simultaneously—by net asset value, number of participants, and length of operation—the example of OTP Pension NPF is illustrative.

OTP Pension NPF has been operating in Ukraine since 2009 and enables individuals to build additional pension savings through an investment-based mechanism.

As of March 31, 2026, the fund is the largest open-ended NPF in Ukraine by net asset value (UAH 871.4 million) and by number of participants (66,662 individuals). The fund’s average annual return over its entire operating period exceeds 14.5%, reflecting long-term effectiveness rather than short-term performance.

The fund is part of OTP Group, a European financial group with a multi-layered risk management system and transparency standards typical of EU financial markets.

Should you choose an NPF based only on returns?

Returns matter, but they are not the only criterion. Evaluating a fund over a short period can be misleading, as high one-year results may stem from an aggressive strategy or temporary market conditions.

For pension savings, what matters most is not peaks but stability, risk control, and consistent results.

Therefore, the more appropriate question is: which fund offers the best combination of stability, transparency, experience, performance, and convenience for me personally?

Why NPF returns may fluctuate

An NPF invests participants’ funds in financial instruments. The value of these instruments can change depending on market conditions, interest rates, inflation, bond yields, currency fluctuations, and other factors.

This is normal for an investment product. What matters is that the fund follows a clear strategy, complies with legal requirements, and operates in the long-term interests of its participants.

Which NPF to choose: depending on your situation

If you are just starting to save

Simplicity is key: clear onboarding, a low entry threshold, the ability to make small contributions, straightforward information on the website, and access to a consultant.

If you plan to contribute regularly

Pay attention to how convenient it is to make contributions. For pension savings, regularity is often more important than the size of the initial contribution.

If you are 35–50 years old

It is worth assessing how many years remain until your desired payout age, how much you can set aside, and what level of future pension income you aim to achieve.

If you are an employer

An NPF can be part of a social benefits package. For corporate programs, fund reliability, clear administration, HR support, and transparent reporting are essential.

How to check an NPF before signing a contract

- Find the fund’s official website

- Verify the administrator, asset management company, and custodian bank

- Assess the fund’s assets

- Review the number of participants

- Examine returns over several periods

- Evaluate transparency of information

- Check how contributions are made

- Ask questions to a consultant

- Understand payout conditions

- Compare several funds

Conclusion: which NPF to choose

When choosing a non-state pension fund, do not look only for the highest returns. Look for a fund you are willing to trust with a long-term financial goal.

A good NPF should be clear, transparent, stable, convenient, professionally managed, and open in its communication.

Such a fund does not rely on a single strength but on a balanced combination of factors: operating history, assets, participants, transparent reporting, professional management, user-friendly service, and open communication.

In other words, a good NPF is not one that merely describes itself well—it is one that can be verified by facts.

Pension saving is not a one-day decision. It is a financial habit that works when you act systematically.

Start with the basics: compare several NPFs, review their results, assess the convenience of contributions, and ask yourself the key question—am I ready to entrust this fund with my long-term pension savings?

Frequently asked questions about Non-State Pension Funds

What is an NPF and why is it needed?

A non-state pension fund (NPF) is a financial instrument for long-term accumulation of funds for an additional pension. Participants make voluntary contributions (individually or through an employer), and the fund invests these assets in accordance with the law.

Unlike the state pension system, savings in an NPF are:

- personalized—funds are recorded in an individual account;

- independent of demographic factors;

- formed as personal financial capital for the future.

How does a Non-State Pension Fund work?

The NPF mechanism includes several stages:

- The participant or employer makes pension contributions.

- Funds are credited to an individual pension account.

- Assets are invested by the asset management company in permitted financial instruments.

- Investment results are reflected in the value of pension savings.

- Upon meeting the specified conditions, the participant receives pension payments.

Importantly, funds do not remain idle—they work in the economy, generating long-term results.

How is an NPF different from other saving methods?

Key differences include:

- a focus on 20 years or more, rather than short terms;

- an investment-based nature rather than fixed interest;

- special regulation and multi-level oversight;

- a clear purpose—pension payouts.

That is why NPFs should not be compared solely with deposits or simple “money storage”; they are instruments of a different class.

How secure are participants’ funds?

An NPF operates within Ukrainian legislation. Management functions are divided among the administrator, asset management company, and custodian bank, each performing a distinct role, which reduces operational risk.

NPF assets do not legally belong to the management company or administrator; they belong to the participants and cannot be used to cover other parties’ obligations.

This separation of responsibilities and regulatory oversight reduces operational and legal risks for participants.

How should NPF performance be evaluated?

Because an NPF is a long-term instrument, one-year results are not indicative. Consider:

- performance over extended periods;

- dynamics of pension unit value;

- consistency of investment strategy;

- fund scale and number of participants.

A one-year snapshot without context does not provide a full picture.

What is the minimum contribution amount?

There is no legally fixed minimum contribution. The amount is determined by the specific NPF’s terms and the pension contract.

The key principle is accessibility and flexibility, not a large initial capital. What matters more than the first contribution size is:

- regularity of payments;

- duration of participation.

Time and consistency—rather than a large upfront amount—drive meaningful long-term results.

How to choose a Non-State Pension Fund?

When selecting an NPF, evaluate:

- operating history;

- asset size and growth dynamics;

- quality and regularity of public reporting;

- reputation of the asset management company;

- alignment with your financial goals and time horizon.

The question “which NPF is best” has no universal answer—it depends on individual expectations and context.

Is there a “the best” NPF in Ukraine?

There is no single best NPF. Funds differ by:

- scale;

- investment strategy;

- history and governance structure.

The best fund for a given participant is one that demonstrates stable long-term results and operates transparently.

Does an NPF guarantee returns?

No. An NPF is an investment product, and returns are not guaranteed. Results depend on market conditions, inflation, interest rates, and asset management quality.

At the same time, legislation sets limits on risk and investment structure to protect pension savings.

Why do returns change fromyear to year?

Annual results may fluctuate due to:

- changes in market rates;

- fluctuations in securities prices;

- macroeconomic factors.

For pension savings, long-term outcomes matter more than individual years of high or low returns.

Can you change an NPF after signing a contract?

Yes. Legislation allows you to:

- transfer pension savings to another NPF;

- stop making contributions;

- receive payouts in cases предусмотрені by law.

Choosing which NPF to work with is your right, supported by legal transfer options.

At what age should you start saving in an NPF?

The earlier, the better. Even small contributions over a long period can yield significant results due to the effect of time in investments.

That said, starting later in life is also possible—regularity and planning horizon are what matter most.

Who is participation in an NPF suitable for?

NPFs suit people who:

- plan their financial future years ahead;

- do not rely solely on the state pension;

- understand the value of regular saving and time in investing.

The starting age is individual, but the longer the horizon, the greater the accumulation effect.

Is an NPF suitable for employers?

Yes. NPFs are often used as part of employee benefit packages, serving as a long-term motivation tool that enhances staff loyalty and financial stability.