OTP Capital: View on the current events

Dear members of OTP Pension Fund, we understand your concern about the results demonstrated by OTP Pension fund over the last month. Therefore, we decided to give you a detailed commentary on the results presented and explain how the fund works, where it invests, why it chooses such a strategy and what the investors should expect in the nearest and distant future.

Let’s start with the irrelevant. Non-state pension fund is, first of all, a financial tool. In addition, if we talk about NSPF in this regard, the fund is a portfolio consisting of various assets. Given that the primary purpose of any NPF is to retain and multiply the accumulation of its participants, most funds follow a conservative investment strategy, by choosing fixed income tools with minimal risk and by complying with maximum asset diversification.

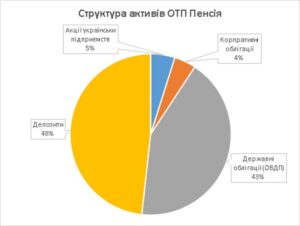

Now directly about the OTP Pension fund. The strategy of OTP Pension fund involves the investment in the most reliable and at the same time sufficiently profitable tools: ins top bank deposits, government and corporate bonds, and a very small part in the share of Ukrainian corporations. You can see the current structure of the fund’s assets below.

Today, the fund’s portfolio consists of sufficiently conservative tools, namely a 48% deposit share, which is distributed among the seven highest quality banks. Another part of the fund’s investments (43%) are government bonds (G-bonds) with different payment periods, from 1 to 5 years. A very small part of assets is invested in shares – 5%, and corporate bonds – 4%.

More about each asset class:

– Bank deposits. When placing deposits with a particular bank, OTP Capital is guided by the sufficiently rigid principle of diversification, namely – not more than 10% of investments in one bank. Banks that hold OTP Pension’s cash go through a multi-level and very rigid OTP Group risk management system, and only after successful audit results, the cash is placed in one or another banking institution. Consequently, in more than 10 years of operation of the pension fund and two powerful financial crises, there was no case when a deposit was not returned to OTP Pension.

In the current situation, 48% of assets of the fund placed on bank deposits are a kind of safety net, which yields a sufficiently high income to the fund’s depositors, as the average deposit rate is about 18%.

– Shares. OTP Pension portfolio includes 2 shareholdings, Ukrnafta (1%) and Raiffeisen Bank Aval (4%). Both Raiffeisen and Ukrnafta’s shares are fundamentally high quality and profitable, and we expect them to pay significant dividends in 2020. In the March crisis, their value decreased by 13% for Raiffeisen and 17% for Ukrnafta, although in the previous period, in February, these shares showed very active growth (Raiffeisen rose by 9% and Ukrnafta by 17%). That is, the fall in prices in March simply offset the increase in February. This is a natural state of thing, as the stock prices react quite sensitively by falling in times of uncertainty in crisis periods. It is worth noting that the impact of the shares on the fund’s portfolio is not significant, as their part is only 5%. Despite the decrease in value, we continue to hold these assets with the expectation of dividends, and therefore the value of a share at one time or another is not critical within the given investment.

– Corporate bonds. In this asset class, OTP Pension holds only 4% in UkrPoshta bonds. These bonds yield OTP Pension depositors more than 20% of profit per year. UkrPoshta has been very carefully inspected by the risk management of the OTP Group for potential waiver. As a result, the conclusion on UkrPoshta is positive and is influenced by the following factors: the company is state-owned, the issue of bonds is insignificant, the management of UkrPoshta is successfully reforming, the company finished 2019 with a sufficiently high profits.

– Government bonds (G-bonds). G-bonds are the most reliable tool in the Ukrainian financial market, as the borrower is the state. Moreover, it is absolutely futile for the state to waive, especially in UAH. In the structure of the OTP Pension portfolio, G-bonds occupy a significant share part – 43%. In these 43 percent, there are 11 issues of government bonds with different maturities, from 1 to 5 years. That is, in the least risky tool, there is an additional diversification, which also reduces the risks of investment.

However, despite the minimal risk, the government bonds were the cause of the poor results of OTP Pension in March.

What is the matter? The matter is that it is in March when the yield of government bonds was quite variable – it was increasing and then decreasing, because various transactions were made on the secondary market with yields ranging from 10% per annum at the beginning of the month to 22% per annum at the end of the month. This is also a common pattern for a crisis period. However, what does OTP Pension have to do with it? In order to understand the answer to this question, it is necessary to understand how the fund’s assets accounting is made. First of all, according to the international standards and world practices, fund assets should be valued at their market value so that fund participants could understand the real value of their savings, and not the paper one. Such revaluation of assets is conducted on a daily basis. For the purpose of revaluation of government bonds, we take the value of bonds published by the NBU on its website. The NBU, in response to the large volatility of interest rates on the secondary market, increased the yield of bonds from 11% per annum at the beginning of the month to 19% per annum at the end of the month. Increasing yields on bonds always lead to a fall in the price of such bonds, and the longer the term to its maturity, the greater the fall in price (for more information, the issue theory – see via the link). In simple words, if a fund has purchased a bond of UAH 100 with annual yield of 10% and maturity in December 2020, then, at the end of the period, it will receive UAH 100 + 10% of yield, i.e. UAH 110. Correspondingly, by making calculations every day, a fund calculates in its portfolio UAH 100 + 10%/365 (yield for a particular day).However, if bond yields increase, then it affects the price by decreasing it. And now the fund should account for 20% of the yield on a bond, which decreased in cost to UAH 91.67. (100/1.2). As a fund keeps a record of government bonds at book value (at cost), such a fall has a negative but temporary effect on the volume of assets. But, in fact, by holding government bonds to maturity, a fund will still receive its UAH 110, as UAH 91,67 + 20% of the yield equals to UAH 110. Therefore, here is the explanation of why the fund reacted negatively to the increase in interest rates on government bonds. After all, the yield of government bonds will remain unchanged and will yield to their owners the profit that was embedded in the bond itself. The current drawdown is the result of a revaluation of an asset at a particular point in time, which does not affect the internal yield of the bond itself, if held to maturity. Given that the fund’s portfolio currently operates at 18% per annum, by the end of the year, OTP Pension’s portfolio will yield about 8% per annum of net yield.

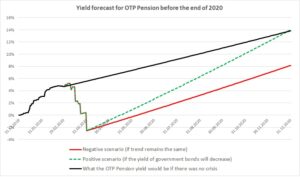

Given the above data, we would like to demonstrate the possible scenarios for the situation development. Below is a graph showing the results of the fund’s activities: a) in case of negative scenario, i.e. if the situation remains as it currently is; b) in case of positive scenario, if the situation stabilizes and the yield of government bonds decreases; and c) scenario, in case of which the portfolio would work under normal conditions, if there was no crisis.

Yield forecast for OTP Pension before the end of 2020

In addition to the yield currently pledged in the portfolio, the additional source of incomes for OTP Pension may be a decrease in yields on government bonds, which is unambiguous. The IMF assistance allows the additional monetary stimuli from the NBU. In the conditions of stabilization of the financial situation in the economy of Ukraine, the National Bank will continue the policy of cheap money in order to ease the cost of lending to revitalize the country’s economy, in particular, by further reduction of the discount rate. Reduction of the financial resource cost in the country will also stimulate the decrease in yields on government bonds, which will immediately reflect on the additional increase in the value of government bonds in the fund’s portfolio, and then, by the end of the year, OTP Pension will be able to yield more than 14% to its depositors, which will offset all the March losses, and will allow to reach the planned in 2020 yield and to flush the “Black March”.